During the last several months, I have been hearing the same worried question over and over from business leaders trying to apply their new business acumen skills and tools, “Should we be worried about inflation?”

leaders trying to apply their new business acumen skills and tools, “Should we be worried about inflation?”

The answer is not just yet. But let’s recheck this in February after all the Christmas and holiday sales have flushed through the system.

According to the US Bureau of Labor, the Consumer Price Index (CPI) for all urban consumers increased 6.2 percent from October 2020 to October 2021, the largest 12-month increase since the period ending November 1990. Prices for all items less food and energy rose 4.6 percent over the last 12 months, the largest 12-month increase since the period ending August 1991. Those numbers are definitely worrisome. Energy prices rose 30.0 percent over the last 12 months, and the food index increased 5.3 percent. If you remember sleeping in your car to get gas in the 1970s, then those numbers should terrify you.

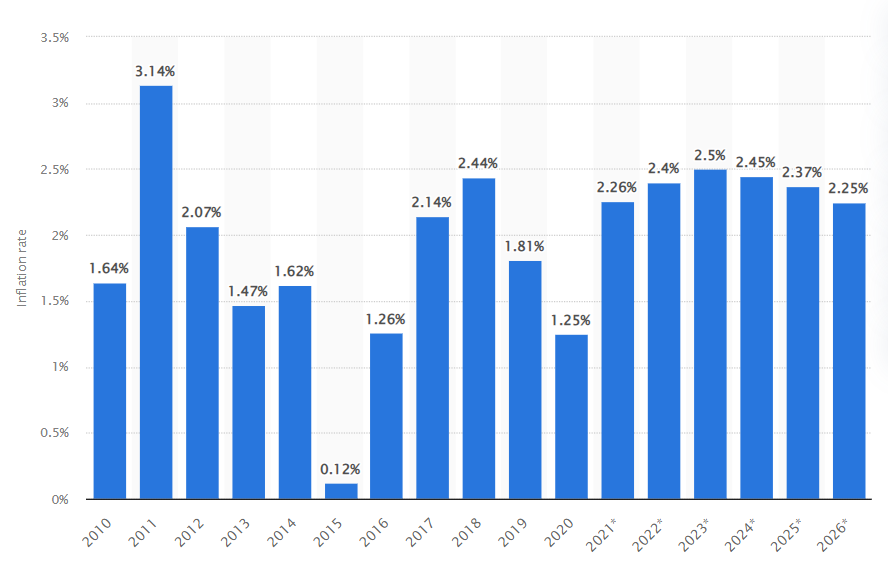

Based on many different economic forecasts, the inflation rate is supposed to level out around 2.5% next year and then be in the range of about 2.25% over the next few years. Which is high but probably manageable.

It’s going to depend on the labor markets

Traditionally, growth pressures and inflation pressures slow down when the unemployment rate goes down. And usually, a small increase in interest rates does the trick and settles everything down. Unfortunately, there are some big misconceptions about that in the “new normal” of the post-pandemic economy. I think the biggest issue is that there are 10.4 million job openings despite the unemployment rate being at 4.2%. Think of it this way, if every unemployed American (6.9 million) took an open job, there would still be 3.5 million openings.

There is still a lot of pent-up demand for both investments and consumption. Even with new entrants, the labor market is going to remain extremely tight for some time and workers will take advantage of that in a post-pandemic economy. Even as price inflation initially slows down, wage inflation will continue to pick up. It may build slowly but lead to wage-price dynamics with more momentum than the price inflation due to supply chain issues. And inflation may be hard to stop without a large increase in interest rates by the Federal Reserve.

There is no doubt that the Federal Reserve will have to step in and raise interest rates to slow down the inflation. Based on past history, it will probably be 2-3 months too late. The questions business leaders will need to think about are: How much will the Fed have to increase interest rates, and for how long? Markets seem completely calm as the real 5-year rates are close to minus 2 percent. Which doesn’t make sense given the employment situation.

As a student who was in business school studying finance in the 1980s, I can share that the history lessons we should look at now are episodes of disinflation.

If you remember, or feel like looking it up, there is a lot of relevance to the Paul Volker (former Chairman of the Federal reserve) disinflation programs of the early Reagan 1980s and its large output costs. Are things different today? One difference is that George H. W. Bush kept things steady after Reagan left office. Today, Joe Biden is changing everything Trump did and these changes will have a major impact. How would a sharp and largely unanticipated increase in rates affect not only the economy but also the financial system, and the prospects for emerging markets and markets that are trying to make a comeback?

This is what business leaders should worry about.

This is not the time to fight about inflation between the short term and the long term. It is also not the time to pretend that everything is okay. If things break poorly, we could be on the verge of unprecedented hyperinflation. If you are a business leader trying to understand what the immediate future looks like, it is the time to think about what happens if inflation turns out to be higher and harder to fight than the Biden administration and the Fed expected.

If that happens, there is definitely plenty to worry about.